Nvidia at $200: Is It Time to Buy Before $300?

2026-07-07

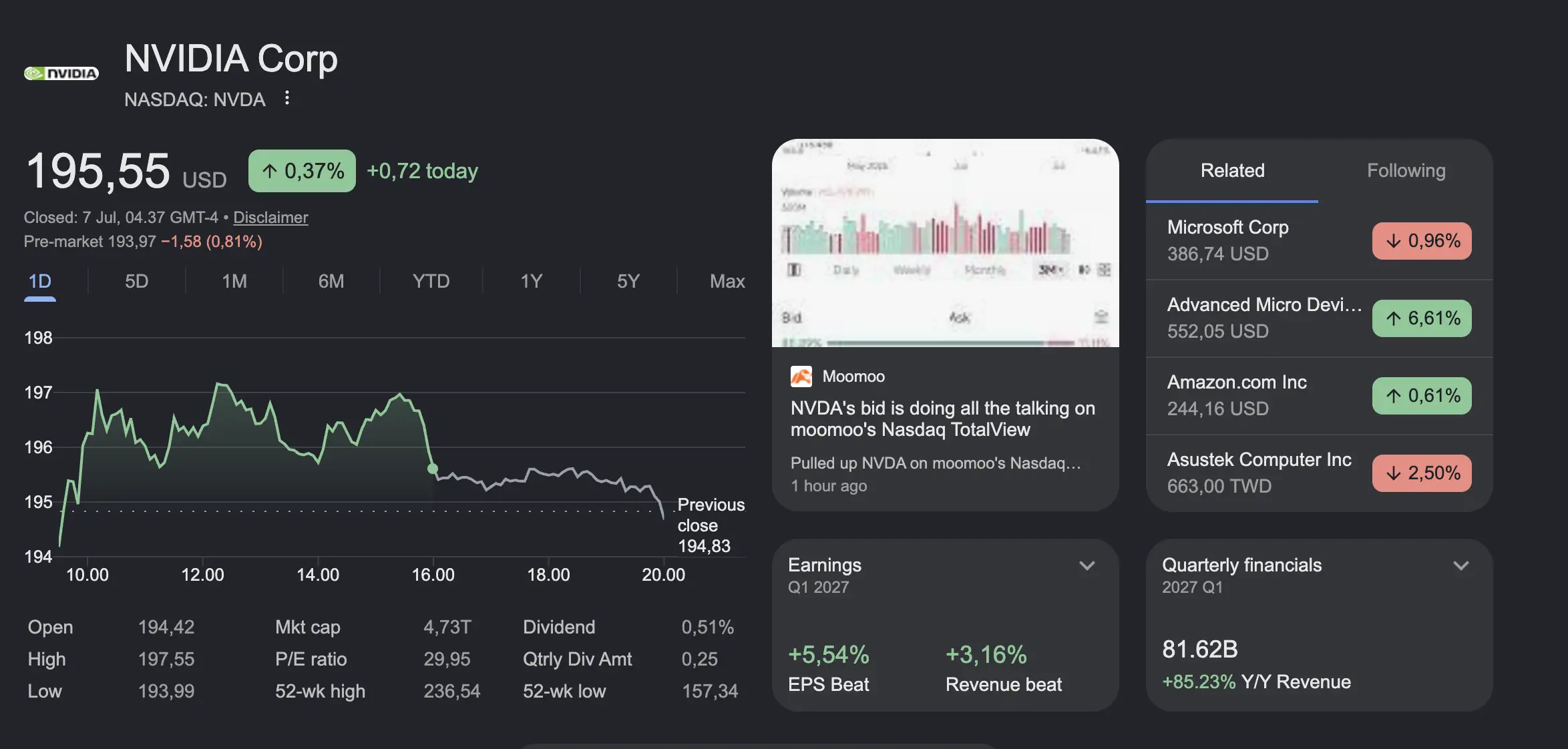

Nvidia (NASDAQ: NVDA) is currently trading below $200 per share, down 16% from its highs and up just 5% through 2026, lagging far behind the S&P 500, which is up nearly 10%.

For investors accustomed to strong returns in 2023-2025, this performance is disappointing and raises the question: is this the time to get out, or is it the best time to buy before the price soars to $300?

Despite concerns about AI overspending, Nvidia's fundamentals remain strong with projected revenue growth of 82% in 2026 and 41% in 2027.

With a valuation now on par with the market average, Nvidia offers an attractive opportunity for long-term investors.

Key Points

Nvidia (NVDA) is currently trading below $200 per share, down 16% from its highs and up only 5% in 2026, lagging the S&P 500 (+10%).

With a PE of 21.7x (equivalent to the S&P 500), Nvidia's valuation is relatively cheap considering its projected revenue growth of 82% in 2026 and 41% in 2027.

A price target of $300-$319 by the end of FY2028 (January 2028) is still realistic, with a potential upside of 50% in the next 18 months.

Interested in exploring US stocks and other digital investment opportunities? Register at Bittime Now, trade crypto and digital assets safely and reliably in Indonesia!

Why Did Nvidia Drop Below $200?

Source: Google Finance

Nvidia's drop below $200 was triggered by market concerns about overspending by AI hyperscalers.

The four main hyperscalers (Amazon, Microsoft, Google, Meta) is expected to spend approximately $650 billion on data center capital expenditures in 2026, and is projected to reach $1 trillion in 2027.

However, hyperscalers themselves have repeatedly stated that the risks of underspending far outweigh those of overspending, indicating their commitment to AI infrastructure expansion remains strong.

These overspending concerns sparked a sell-off across AI-related stocks, and Nvidia was no exception.

However, this decline actually creates an opportunity for investors who believe in Nvidia's long-term prospects, given that the company's core business remains healthy and GPU demand continues to rise.

Read also:Buy US Stocks via Crypto, Get 7% Daily Rewards at Bittime

Why is Nvidia Still Attractive?

Despite the depressed stock price, Nvidia's fundamentals remain solid.

The company designs GPUs and a complete product ecosystem that hyperscalers and cloud providers rely on.

Once clients choose the Nvidia ecosystem, they tend to stick with it because of the deep integration and high switching costs.

NVDA PE Ratio (Forward) data by YCharts.

Nvidia's valuation is also a major draw. Currently, Nvidia shares are trading at 21.7 times forward earnings, on par with the S&P 500.

This means the market is treating Nvidia as an average stock, even though Wall Street analysts are projecting revenue growth of 82% in 2026 and 41% in 2027, well above the market average.

In other words, Nvidia's future growth is not yet fully reflected in the current stock price.

Additionally, Nvidia has a dominant position in the ever-growing AI GPU market.

With hyperscalers' capital spending continuing to increase, demand for Nvidia products is certain to remain high in the coming years.

This provides a strong foundation for the company's revenue and profit growth.

Read Also:US Stock Tokenization: Hold Your Favorite US Stocks and Get Rewards Every Day

Nvidia Price Projection to $300

To reach $300, Nvidia needs to see a rise of about 50% from current levels.

Based on analyst projections, Nvidia's earnings per share (EPS) for FY2028 (ending January 2028) is expected to reach $12.76.

Assuming a 25x PE valuation (which is still lower than Nvidia's average PE in recent years), the stock price target is $319.

This target could be achieved by the end of FY2028, providing an upside of around 50% in about 18 months.

This is a very attractive return in a relatively short period of time.

Additionally, analysts have tended to underproject Nvidia's growth, so actual EPS could be higher than projected, potentially pushing the stock price even higher.

Another supporting factor is that much of this growth was already predictable as Nvidia management likely had good information about customer orders for the year ahead.

Thus, the risks to this target are relatively limited.

Read Also:Tokenized Stocks vs. Regular Stocks: Definition, Differences, and How to Buy

Conclusion

Nvidia's drop below $200 creates an attractive buying opportunity for long-term investors.

With strong market dominance, solid revenue growth, and a low valuation, Nvidia has the potential to reach $300 in the next 18 months.

For investors who believe in the prospects of AI and the adequacy of hyperscalers' capital spending, the current downturn is a good time to accumulate shares before the next rebound.

Bittime is a licensed and regulated Digital Financial Asset Trader (PAKD) supervised by Indonesia’s Financial Services Authority (OJK) — where you can buy Bitcoin in Indonesia and hundreds of other crypto assets starting from just Rp10,000. The registration process is fast, secure, and you can get started today.

Track USDT to IDR conversions and monitor your favorite crypto assets in real time. Everything is available in one crypto investment app that you can download for free on the Play Store

Ready to start? Register now on Bittime and execute your investment strategy with a platform trusted by millions of users in Indonesia.

FAQ

How much does Nvidia cost now?

Nvidia is currently trading below $200 per share, down 16% from its high.

Why is Nvidia down?

The decline was triggered by concerns about overspending by AI hyperscalers and a sell-off in AI-related stocks.

Is Nvidia still a good stock?

Yes, with projected revenue growth of 82% in 2026 and 41% in 2027, and a PE of 21.7x which is equivalent to the S&P 500.

What is Nvidia's price target?

Analysts project a target of $319 based on EPS of $12.76 and PE of 25x in FY2028.

When will Nvidia reach $300?

It is predicted to reach $300 by the end of FY2028 (about 18 months ahead).

What are Nvidia's main risks?

The main risks are a slowdown in hyperscalers' capital spending or competition from AMD and other AI chip companies.

What are Nvidia's advantages over competitors?

A complete product ecosystem and deep integration with customers create high switching costs.

Disclaimer: The views expressed belong exclusively to the author and do not reflect the views of this platform. This platform and its affiliates disclaim any responsibility for the accuracy or suitability of the information provided. It is for informational purposes only and not intended as financial or investment advice.

.png)